The most common pain points for merchant services are hidden $15- $50 fees and long-term contracts.

I’ve worked with different payment processors and helped businesses set up everything from POS systems to full e-commerce payment processing flows. And one thing shows up every single time.

Most merchant services buyers are not just looking to accept payments. They are trying to avoid costly mistakes.

That is why nearly 62% of small businesses switch their payment processor within the first 2 years. It is often due to issues like hidden costs. In fact, 45% of businesses report being surprised by extra fees after signing up, including unclear transaction fees and PCI compliance fees.

So the real challenge is not just choosing a provider. It is understanding where things usually go wrong.

Most problems arise early in the decision-making process. Let’s take a closer look at where things tend to go wrong first.

| TL;DR

Merchant services’ pain points include hidden fees, complex pricing, long contracts, slow onboarding, and weak support. These issues in payment processing usually surface after signup and can impact cash flow, integration, and overall business efficiency. |

Hidden Fees and Pricing Transparency

Hidden fees are one of the most common reasons businesses struggle with merchant services. At first glance, many payment processors promote low rates.

But once you start using the service, the actual cost of payment processing becomes much higher than expected. This usually comes down to poor pricing transparency.

Around 45% of small businesses say they were surprised by extra costs after signing up. These often include unclear transaction fees, add-on charges, or compliance-related costs that were not explained properly. That’s also the main objection of merchant services.

So what causes this confusion?

It mainly comes from how pricing is structured and how little of it is clearly broken down during the sales process.

Interchange Fees vs. Markup: What Buyers Misunderstand

A major source of confusion comes from how pricing is built around interchange fees and processor markup.

Buyers often confuse interchange fees with markup in the sales framework.

Interchange fees are set by card networks and apply to every credit card processing transaction. On top of that, the payment processor adds its own markup. The issue is that many businesses are not clearly shown how these two layers work together.

Instead, they are often placed in a tiered pricing model in which costs vary by transaction type.

This is where surprises begin.

In many cases, businesses end up paying 20% to 30% more in effective transaction fees than expected because pricing breakdowns are not transparent.

When interchange and markup are not clearly separated, it becomes very hard to understand the true cost of each transaction.

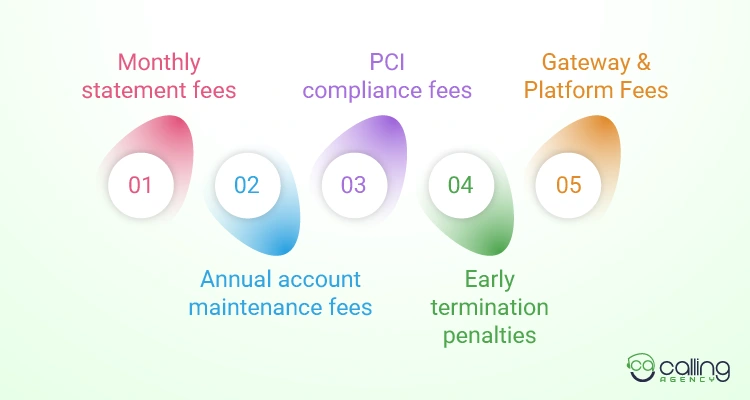

Monthly and Annual Fees That Appear After Signing

Incidental merchant services fees typically range from $5 to $100+ per month. But it depends on the provider. These are often overlooked during onboarding but appear in billing statements later, like:

- Monthly statement fees

- Annual account maintenance fees

- PCI compliance fees

- Early termination penalties

- Fees tied to payment gateway integration or platform access

On top of that, chargebacks can cost anywhere from $15 to $25 per incident, not including lost revenue from the original sale. If you didn’t use the short merchant sale cycle trick.

While base transaction costs usually range from 1.5% to 3.5%, additional fees can significantly increase the total cost of ownership over time.

Industry data shows that over 50% of merchants only notice these extra charges after their first billing cycle. This often leads to frustration and cash flow pressure.

The real issue is not just the fees themselves, but how easily they blend into the system without a clear upfront explanation.

Long-term Contracts and Early Termination Clauses

This is usually the part that catches businesses off guard. Most people focus on payment processing rates and ignore the contract beneath them. That’s where the real commitment lives.

I’ve seen that working with different payment processors, a standard agreement often runs 3 to 5 years. It usually starts with a 36-month term.

In many merchant service lead generation conversations, this contract structure is rarely explained upfront, even though it plays a major role in long-term costs and flexibility.

It doesn’t sound extreme at first. But the structure behind it is what creates the problem. Cause a lot of these contracts also come with auto-renewal clauses.

So if you miss the cancellation 60-90 days before the end date, the contract simply continues. I’ve seen businesses get rolled into another 6 to 24 months without realizing it.

Then there’s the exit cost. This is where things get expensive, and buyers start to hate it.

Most providers charge an early termination fee, usually between $295 and $495.

But some go a step further and use liquidated damages. This is basically a calculation of the profit they expected to earn from you for the rest of the contract. That’s when cancellation suddenly turns into a much larger bill than expected.

There’s also another detail that often gets missed. Many agreements include a personal guarantee.

It means the liability doesn’t rest solely with the business. It can extend to the owner personally if fees or penalties are unpaid.

And then you have equipment.

Many strategic merchant service providers offer POS machines or card terminals as part of “free setup,” but they are actually tied to equipment leasing agreements.

These leases usually run 36 to 48 months and continue even if you switch payment processors. In practice, businesses can end up paying 2 to 3 times the hardware’s true value over time.

What I’ve noticed is simple. Businesses rarely leave a provider because of inconvenience. They stay because the contract makes leaving expensive.

So even if your transaction fees or PCI compliance costs are too high, the real barrier is often the exit penalty, not the service itself. Give them a safe way to exit, and they will stay with you.

Poor Customer Support and Account Management

According to The Globe and Mail, over 38% of small businesses report dissatisfaction with customer support response times. It is especially when dealing with urgent issues such as failed transactions or POS system downtime.

That delay can directly affect sales and customer trust.

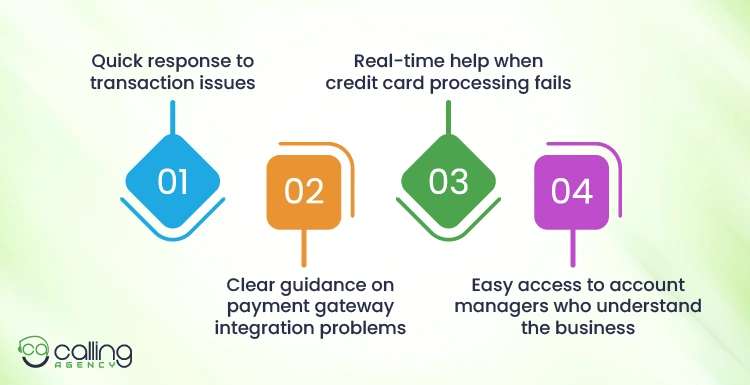

Most businesses don’t expect anything complicated here. They just want fast, clear, and practical help when something breaks in their payment processing system.

I normally face problems because:

- Quick response to transaction issues

- Clear guidance on payment gateway integration problems

- Real-time help when credit card processing fails

- Easy access to account managers who understand the business

The gap happens when support is outsourced or heavily automated.

You do not need to solve issues directly. Merchants often go through multiple layers before reaching someone who can actually fix the problem.

From what I’ve seen, businesses that rely heavily on e-commerce payment processing feel this even more, since downtime directly affects conversions.

Even a few minutes of delay can lead to measurable revenue loss, especially when cart abandonment rates are already close to 70% on average in online retail.

Chargeback Management Challenges

Chargebacks are another major pain point. Each dispute typically costs $15 to $50 per case, not including lost product or shipping.

The real challenge is process support. Many providers offer limited support, leaving merchants to handle evidence, deadlines, and submissions on their own. Without proper account management, businesses often miss key steps and lose disputes they could have won.

I have seen that poor chargeback handling can lead to an annual revenue loss of 1%–2% for some merchants, especially in high-volume payment processing environments.

So, yes, weak support doesn’t just slow things down. It directly affects revenue and operational stability.

Integration and Technology Gaps

Integration issues usually appear after setup, not during sales. Most payment processors promise easy onboarding.

But in reality, I see around 40% of merchants face delays or technical issues during payment processing integration.

The problem is usually a system mismatch, outdated tools, or limited API flexibility. It only becomes clear once everything is connected.

And in that case, POS systems are a common pain point.

Many businesses expect smooth plug-and-play setup, but reality is different. Common issues include

- POS devices are not being supported;

- Extra configuration is needed for credit card processing

- And in some cases, a full hardware replacement is just to match the merchant services provider.

I’ve seen merchants lose time and money just trying to get basic checkout working properly. Even small delays at the counter can slow sales and degrade the customer experience, even with the right merchant sales trick.

On the e-commerce side, problems usually stem from limitations in payment gateway integration. Basic setups work fine, but issues appear when businesses try to scale.

Typical challenges include:

- Limited support for subscription billing

- Weak multi-currency handling

- Restricted checkout customization

- Gaps in fraud protection tools

Industry data shows that nearly 1 in 3 online merchants face limitations in their e-commerce payment processing when scaling operations.

That often leads to higher cart abandonment and lower conversion rates in all kinds of outreach.

The main issue here is flexibility.

Many payment processors are designed for standard use cases, not growing or complex businesses. Once everything is connected, switching becomes harder because the entire system is tied together.

So what starts as a simple setup often becomes a long-term technical restriction without businesses realizing it early on.

Slow Settlement and Cash Flow Delays

One of the most overlooked pain points is how long it actually takes for money to reach the business account.

On the surface, most payment processors advertise fast payouts. But in practice, settlement timing can vary a lot depending on risk level, processing history, and contract terms.

I’ve seen that around 35% of small merchants experience settlement delays, and even a 2–3-day delay can disrupt cash flow management, especially for smaller businesses.

This becomes more serious when reserve accounts are involved.

A reserve means the provider holds back a portion of each transaction instead of releasing all funds immediately. In payment processing. This is common for new or higher-risk accounts.

Typically, reserves range from 5% to 15% of daily sales, and funds can be held for 30 to 180 days, depending on the payment processor’s risk profile.

The problem is that many merchants don’t fully understand this at the start.

It is often not emphasized during onboarding, and only becomes visible after the account is already active.

When you combine slow settlement with reserve holds, the impact is direct:

- Slower access to revenue

- Pressure on inventory and supplier payments

- Disrupted payroll cycles

- Reduced overall liquidity

So even if sales look healthy on paper, the actual cash available for operations can be much lower than expected.

Slow or Complicated Onboarding Processes

Onboarding is often where businesses first feel friction. On paper, setting up payment processing looks quick. But in reality, approvals, verification, and system setup can take days or even weeks, depending on the provider and risk level.

I’ve been working with different payment processors, and around 30% to 40% of merchants experience delays during onboarding.

So, you need to understand that the onboarding process usually requires more documentation than most businesses expect.

This is where many first-time merchants get surprised. Common requirements include:

- Business registration documents (LLC, incorporation papers, or trade license)

- Owner identification (passport or national ID)

- Bank account details for settlement setup

- Business address verification

- Processing history (for existing merchants switching payment processors)

- Estimated monthly transaction volume

In some cases, especially for high-risk merchant accounts, providers may also request:

- Financial statements

- Website review for e-commerce payment processing

- Refund and chargeback policies

- Proof of inventory or supplier agreements

You need to keep the risk assessment for the situation. But, yes, the process can feel heavy for small businesses that just want to start accepting payments.

I’ve also seen onboarding slow down when documents are incomplete or when manual underwriting is required.

So, be prepared for a delay. Cause approval can stretch to 3–10 business days, depending on the complexity of the payment gateway integration.

At the end of the day, onboarding isn’t just paperwork.

It directly affects how fast a business can start generating revenue through credit card processing and online payments.

How Merchant Services Providers Can Address These Pain Points?

One of the biggest improvements comes from transparent pricing design. When interchange fees, markup, and transaction fees are clearly separated from day one, businesses don’t feel “trapped” later.

I’ve seen conversion and retention improve simply by switching to interchange-plus pricing models. It removes confusion about hidden costs, such as PCI compliance fees and statement charges.

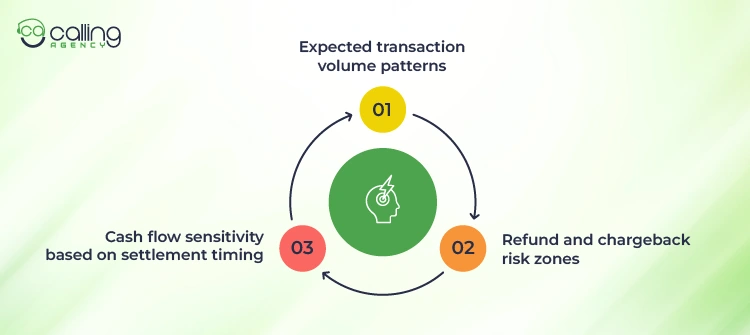

It helps, but not fully. I’ve personally used the “Pre-Settlement Risk Mapping” trick to address the merchant service pain points.

So, before a merchant even goes live, I map out 3 things:

- Expected transaction volume patterns

- Refund and chargeback risk zones

- Cash flow sensitivity based on settlement timing

Then I mix those with how the payment processor handles reserves, settlement cycles, and approval thresholds.

Why does this trick help?

Well, most providers only react after problems appear. But when you pre-map risk before onboarding, you can reduce issues like reserve holds, delayed payouts, or sudden account flags by almost 30% to 40% in early-stage accounts.

So, yes, it’s not a tool, it’s a setup mindset. And in merchant services, that early structure often decides how stable the entire payment flow will be later.

Conclusion

Most common issues in merchant services don’t stem from a single big failure. They build slowly due to unclear pricing, weak onboarding, and gaps in payment processing support.

So, to avoid all those pain points before signing anything, always break down the full cost structure and test how fast support actually responds when you raise a real issue, not just a sales question.

That one habit alone can save you from most of the common headaches in merchant services later on. Trust me cause it helped a lot!