You put your heart and soul into your mortgage business every day by building strong client relationships, sharpening your expertise and overcoming the challenges that come your way.

But what if all that effort could unravel in an instant?

That’s the risk non-compliance brings. In the industry, failing to follow the rules of mortgage compliance guidelines isn’t just a minor hiccup. Instead, it’s a threat to everything you’ve worked for. Hefty fines, legal battles, a damaged reputation, and even the loss of your license are the stakes when compliance is overlooked.

Mortgage companies aren’t immune to compliance violations. While they may not have as much regulatory oversight as depository institutions, they are still required to comply with many state and federal laws and the cost of violating these laws can be steep.

Compliance is a critical concern for mortgage companies. Understanding the most common compliance pitfalls and having proactive systems in place to manage compliance risk is essential and tackling this challenge efficiently is smart business.

This guide will highlight some of the most common compliance violations mortgage companies face and provide actionable tips to help streamline compliance management processes to minimize risk.

Perceiving the Regulatory Landscape

The mortgage industry operates with a complex web of laws and ordinances. These legislations protect consumers and make sure that their lending practices remain fair.

Urban Development (HUD), the Federal Trade Commission (FTC), and the Federal Deposit Insurance Corporation (FDIC) all provide consumer protections that are associated with home mortgages and the home lending environment. Additionally Key legislations such as the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) are the backbone of mortgage compliance.

While most of the federal regulations originated in the 1960s and 1970s, state regulations have developed over many decades and through various consumer advocacy efforts that evolved from these existing statutes. The primary goal of consumer protections is to establish transparency without interfering with the overarching principles of free market capitalism.

Regulatory agencies maintain oversight to foster the stability of the housing market while ensuring informed decisions and adequate disclosures prior to a consumer’s decision to borrow on a mortgage.

Thus, consumer protections extend both through informational requirements and through some regulations that establish boundaries, and regulate the mortgage borrowing and lending marketplace.

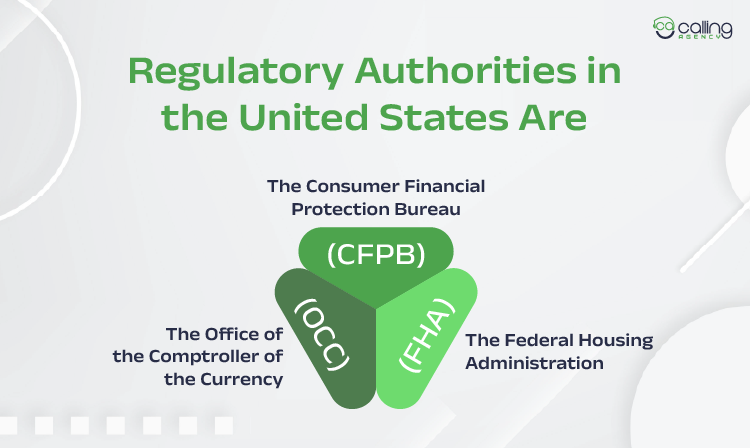

Regulatory Authorities in the United States Are

- The Consumer Financial Protection Bureau (CFPB): This law is responsible for consumer protection in mortgage deals.

- The Federal Housing Administration (FHA): This organization establishes general mortgage standards that include the underwriting process and maximum loan amounts.

- The Office of the Comptroller of the Currency (OCC): The OCC governs and supervises the operations of all national-level banks, federal savings and loan associations and also the branches and agencies of foreign banks located in the United States.

The regulatory landscape is constantly evolving in response to market conditions and emerging risks. As new legislation is introduced or existing regulations are amended, lenders must stay aware of these changes to make sure of compliance.

Some of the factors that have prompted regulatory bodies to reassess existing frameworks and introduce new measures designed to strengthen the industry’s foundation.

- The increasing digitization of mortgage processes.

- Growing concerns about consumer protection.

- Lessons learned from recent market fluctuations.

- The need for greater transparency and accountability.

For instance,

The recent Dodd-Frank Wall Street Reform and Consumer Protection Act conveyed major changes to the mortgage lending regulations. It established the CFPB and introduced new requirements for mortgage pioneers that include reformed background checks and licensing procedures.

Functions of Mortgage Compliance Companies

- Regulatory Guidance and Updates

- Compliance Auditing

- Training and Education

- Documentation and Record Keeping

- Consultancy and Advisory Services

Key Federal Laws Affecting Mortgage Hiring

Over the past years, mortgage brokers have emerged as the principal points of contact between consumers and the mortgage industry. Some brokers have been accused of misinterpreting their clients’ interests, falsifying loan documents and committing fraud.

These accusations have raised doubts about the effectiveness of the existing industry regulation. The costs of predatory lending have been estimated at $9 billion a year over the previous years which created the perception that policy intervention in the form of heightened regulation may be necessary.

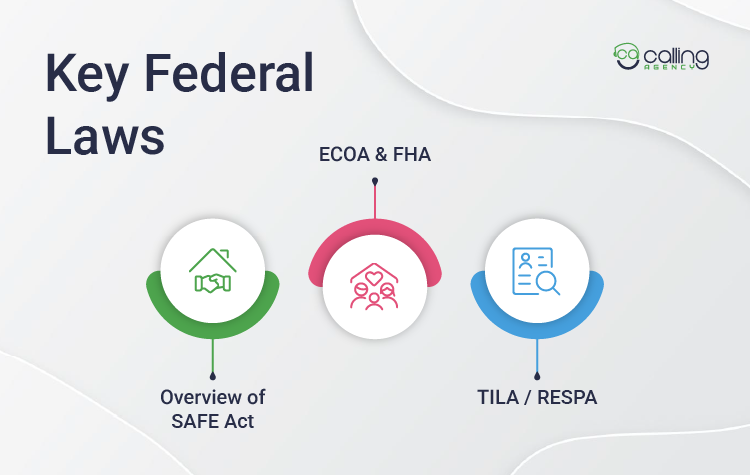

Overview of SAFE Act

Mortgage company employees handle large amounts of money and have access to private information like social security numbers. Consequently, laws exist that require employers to follow certain procedures when hiring mortgage originators.

In accordance with this act, you can only originate loans if you are registered with the National Mortgage Licensing System or a state regulatory authority. Before registering, prospective lenders must complete training classes and examinations that vary by state.

ECOA & FHA

The Equal Credit Opportunity Act (ECOA) is a law that limits discrimination in credit transactions. At the same time, the Fair Housing Act (FHA) is a law that forbids discrimination in housing. Working together to meet compliance requirements and control risks is a partnership that gives clients operating in very regulated environments a sense of security in their operations and strategies.

ECOA applies to businesses and consumer credit that imposes notice and nondiscrimination requirements on all types of credit. Discrimination based on the following is prohibited:

- Sex

- Age

- Religion

- Race

- Marital Status

- National Origin

The FHA applies to any individual whose business engages in transactions related to residential real estate that includes the purchasing or making of loans or offering other financial assistance. Other assistance can be a loan secured by residential real estate or for the purchase, construction, renovation and maintenance.

TILA / RESPA

These were two different laws merged by the Consumer Financial Protection Bureau (CFPB) into one set of rules regarding mortgage disclosure. The TILA-RESPA Integrated Disclosure (TRID) was a step towards making the loan options clearer to consumers. This legislation led to the production of new Loan Estimate and Closing Disclosure forms that consumers get when they apply for and close a mortgage loan.

The Loan Estimate replaced the RESPA Good Faith Estimate (GFE) and the early Truth in Lending disclosure. The rule requires creditors to deliver or place in the mail the Loan Estimate no later than three business days after the consumer submits a loan application.

The Closing Disclosure replaced the HUD-1 Settlement Statement and the final Truth-in-Lending disclosure. The rule requires creditors to ensure that consumers receive the Closing Disclosure at least three business days before consummation.

State & Local Licensing Requirements

No matter where you live and intend to do business in the U.S., becoming a mortgage professional will require you to complete several steps that include completing a pre-licensure course, registering with the Nationwide Multistate Licensing System and meeting other conditions required for licensure.

Personal Requirements

- Being eighteen years of age

- Submit your fingerprints to the FBI and pass a criminal background check (felonies committed in the last seven years or any financial crimes concerning forgery, fraud, bribery, etc. will disqualify you).

- Register with the National Mortgage Licensing System (NMLS)

- Pass the SAFE MLO test

- Submit a credit report

Pre-Licensure Education is the coursework that the state requires before a license can be issued. The education requirements slightly vary from state to state. One common feature is that most of the states will require at least twenty hours of mortgage Pre-Licensure Education.

Take a Mortgage Exam Prep Course

You can choose a course to help you obtain your license. One option is the 20-hour SAFE Comprehensive course, which covers everything you need to know for the licensing exam. This course provides in-depth lessons on essential topics, complemented by engaging activities and resources to further enhance your understanding.

Another option is a specialized exam preparation course. This course focuses solely on practice tests and strategies for taking the exam. It allows you to practice with various questions, helping you feel confident and prepared for the real test.

Pass the SAFE MLO Test

- Register with NMLS and set up an NMLS account

- Complete at least 20 hours of Pre-Licensure Education

- Pass the SAFE MLO Test with a score of 75% or better

- Submit fingerprints to the FBI and pass a background check pre-license (no felonies in the past seven years or any financial crimes concerning forgery, fraud, bribery, etc.)

- Submit to a credit check pre-license

- Complete at least 8 hours of Continuing Education for license renewal each year

Federal law mandates that every mortgage professional must register and adhere to NMLS requirements that include:

- Registering to obtain a unique identifier (every mortgage professional must have an assigned number)

- Paying fees (both federal and state) that cover initial setup costs including background checks, licensing, credit report, and testing along with fees to maintain the license (for a complete list of fees, visit the NMLS website)

- Securing sponsorship, which must be reported when a mortgage professional enters a business relationship with a lender, Mortgage Broker, or lending institution. The Sponsoring Broker will then inform NMLS that they’re supervising the mortgage professional’s licensed activities. Some states require an “Approved Sponsor”, so be sure to check your local laws!

Emerging Compliance Risks in Hiring

Emerging compliance risks include the misuse of AI in recruitment, specifically in cases of bias and fraud, which can lead to discrimination lawsuits and intellectual property theft. Other jeopardies are data privacy, wage and hour violations, identity fraud from scams and non-compliance with regulations like ESG and data protection laws.

Mortgage companies have to follow many rules from both the state and federal government and this can be difficult to handle. If the rules aren’t followed, it means facing issues like legal actions, lawsuits, and penalties.

They include:

Real Estate Settlement Procedures Act (RESPA)

This act mandates lenders to provide homebuyers with accurate disclosures to protect them from abusive practices.

For example, in August 2023, a mortgage company had to pay $1.75 million into the CFPB’s victim relief fund for offering illegal incentives to real estate brokers and agents in exchange for mortgage loan referrals.

Home Mortgage Disclosure Act (HMDA)

HMDA requires mortgage companies to collect and report specific information about mortgages. These companies must keep accurate records of loan applications, approvals, and denials. It’s important to ensure this data is correct and complete to avoid regulatory issues.

In June of 2024, the Consumer Financial Protection Bureau (CFPB) fined a mortgage company $3.95 million for submitting inaccurate HMDA data. That’s after paying a $1.75 million civil money penalty for the same issue in June 2019.

Fair Lending Regulations

Lenders must adhere to legislation preventing discrimination. This covers the Fair Housing Act (FHA) and the Equal Credit Opportunity Act (ECOA). Particularly via the Justice Department’s Combating Redlining Initiative, which defines enforcement guidelines, these laws are rigorously enforced.

The initiative resulted in the second-largest redlining settlement in DOJ history and the first against a non-bank lender when a Delaware-based mortgage company settled a joint DOJ and Consumer Financial Protection Bureau (CFPB) redlining suit for $24.4 million in 2022. The CFPB and DOJ said the mortgage company violated ECOA by actively avoiding making loans and discouraging applicants in majority-minority neighborhoods. As a result, the company generated 50% fewer home loans and 60% fewer applications in these areas than similarly situated lenders.

The following steps will help you manage your obligations:

1. Standardize and localize employment documentation

- Adapt global templates for each jurisdiction

- Create a central repository for version control and compliance review

2. Integrate the payroll and benefits system

- Rely on a unified platform for real-time compliance checks

- Implement country-specific automation for tax and benefits calculation

3. Automate compliance monitoring

- Use AI to track legislative changes

- Set up alerts and dashboards for HR leaders and the compliance team

Mortgage companies are required to comply with many state and federal laws and the cost of violating these laws can be steep.

Pre-Hiring Compliance Checklist

A pre-hiring compliance checklist is a step-by-step tool that helps companies meet all legal requirements and follow their own rules when hiring new employees.

Define Job Descriptions & Requirements

Recruitment, Interviewing, and Hiring

- Create clear and accurate job descriptions that outline essential duties and qualifications.

- Understand the Equal Employment Opportunity (EEO) laws and avoid discriminatory hiring practices.

- Conduct background checks and pre-employment testing following federal and state regulations.

- Provide all the necessary new hire paperwork, including:

- Form I-9: Employment Eligibility Verification form

- W-4: Employee’s Withholding Certificate

- Direct Deposit Authorization Form: For direct deposit of payroll

Onboarding Procedures and Company Policies

- Develop a comprehensive employee handbook outlining all company policies, procedures, and expectations.

- Provide orientation and training programs to educate new hires on your company culture, policies, and procedures.

- Establish clear anti-discrimination and anti-harassment policies, and provide training to all employees.

Employee Classification and Compensation

- Correctly classify employees as exempt or non-exempt based on job duties and responsibilities.

- Adhere to federal and state wage and hour laws, including minimum wage, overtime, and recordkeeping requirements.

Benefits Administration

- Offer required and competitive benefits packages, including health insurance and retirement plans.

- Ensure compliance with COBRA and FMLA regulations for continuation of health coverage and family/medical leave.

Employee Records and Documentation

- Maintain up-to-date employee records, including personnel files, payroll records, and tax documents.

- Implement data privacy and security measures to protect sensitive employee information.

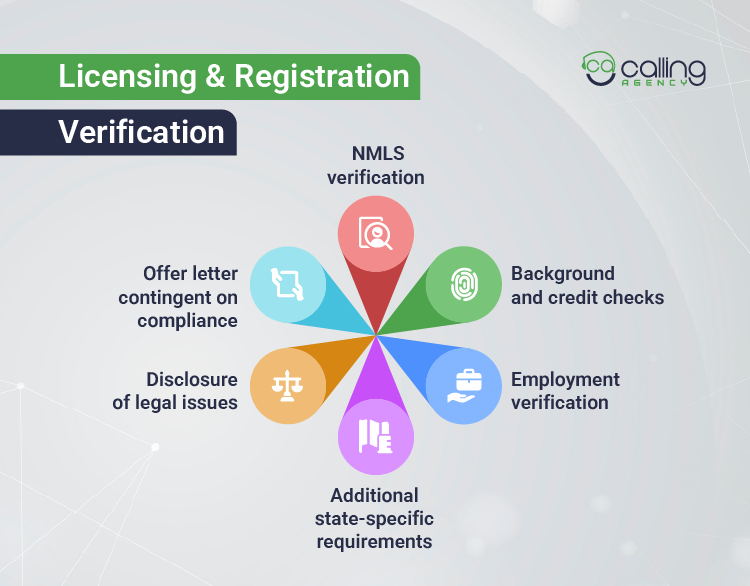

Licensing & Registration Verification

In order to ensure mortgage professionals are compliant, a pre-hiring checklist should definitely comprise of the Nationwide Multistate Licensing System (NMLS) registration as well as the requirements set by the Secure and Fair Enforcement for Mortgage Licensing (SAFE) Act.

It involves making sure that the applicant is the holder of the only NMLS ID and has passed the required national and state-specific tests as well as the pre-licensure education. Additionally, the person must also give permission for a background check and their credit report must be reviewed.

Pre-hiring compliance checklist for mortgage loan originators

- NMLS verification

- Confirm the candidate’s unique NMLS ID.

- Browse the NMLS Consumer Access website to verify the licensing status of the applicant.

- Confirm that the candidate has met the requirement of 20 hours of pre-licensing education with 3 hours each for federal law and ethics and 2 hours for non-traditional mortgage products.

- The candidate must have secured adequate scores, i.e. 75% or above, in the SAFE Mortgage Loan Originator Test.

- Background and credit checks:

- Have the fingerprints of a candidate taken at NMLS offices to facilitate an FBI criminal background check.

- Going through the candidate’s criminal and credit history, it is noted that the person has no flags or regulatory actions.

- Employment verification

- Confirm the candidate’s employment history for at least the past two years to check for stability and consistency.

- Additional state-specific requirements

- Certain restrictive conditions must be met in some states to obtain a license. Make sure to understand and comply fully with the NMLS State Licensing Requirements for each state.

- Disclosure of legal issues

- Help the candidate disclose any administrative, civil, or criminal findings regarding their professional conduct in their NMLS record.

- Offer letter contingent on compliance

- If the candidate passes all compliance verifications successfully and can maintain their active NMLS registration, then make the hiring decision and send the formal offer letter.Background & Credit Checks

Detailed background and credit checks are very important for Mortgage Loan Originators (MLOs) who are licensed. As per the SAFE Act of 2008, MLOs should enlist with the Nationwide Multistate Licensing System (NMLS) and have an in-depth background check carried out. Part of that includes a fingerprint-based criminal check going to the FBI and a credit report evaluation.

If the candidate is a convicted felon of fraud, dishonesty, or money laundering-related offenses during the last seven years, they will be disqualified for life. Although no particular credit score is required, financial situations such as unpaid judgments or bankruptcies could also lead to disqualification. Companies will typically perform these checks on other staff members occupying different roles as well to determine their financial fitness and character.

The Fair Credit Reporting Act (FCRA) is the law that governs the usage of credit and background reports for employment purposes. Employers need to seek permission from the applicants before getting the reports and in case they decide not to employ a person based on the report. They should give the applicant a copy of the report together with a summary of his rights according to FCRA.

Fair Hiring Practices

Fair hiring practices in the mortgage industry involve adhering to regulations set by federal agencies such as the FDIC, CFPB, and EEOC, along with recent updates from the Fair Hiring in Banking Act. These practices aim to eliminate bias, ensure equal opportunity and comply with specific rules.

Key Components Include:

- Updates from the Fair Hiring in Banking Act

- Fair Credit Reporting Act (FCRA)

- Equal Employment Opportunity

- Inclusive Hiring Practices

- Secure and Fair Enforcement for Mortgage Licensing Act (SAFE Act)

Employment Documentation & Onboarding

A pre-hiring compliance checklist for mortgage hiring should include the following steps:

- Verify Employment Eligibility: Ensure that the candidate is eligible to work.

- Obtain Signed Agreements: Collect necessary documents before the employee’s first day. This includes the job offer letter, I-9 and W-4 forms, and consent for background checks.

For the onboarding process, the new hire must complete and submit the following:

- Personal details

- Tax information

- Bank information

- Any necessary non-disclosure or non-compete agreements

By following these steps, you can ensure a smooth hiring and onboarding process.

Training & Ongoing Monitoring

Training for a mortgage involves several steps. First, new employees shadow experienced workers to learn on the job. Then, they watch demonstrations to better understand the process. And then they start their own practice.

Compliance Training for All New Hires

Organizations use detailed training materials, like standard procedures and easy-to-follow documents. They also include training on fair lending, UDAAP (Unfair, Deceptive, or Abusive Acts or Practices), privacy/data protection and monitor them to make sure that the hired people meet both the company and legal standards.

Tools and Resources Include

- SOPs- This ensures that all staff are equipped with essential knowledge needed to operate within the organization

- Internal Resources- Training materials like manuals, e-guide and e-learning modules guarantee learning opportunities for employees.

- Collaboration- Engage with other departments like Quality Assurance and Compliance to make sure that the training is aligned with company policies and regulatory requirements.

- Industry Resources- Continuously monitor current industry trends, regulations and best practices.

Periodic Refresher Training & Updates

Periodically refresher training for mortgage hiring is a mix of different content such as the updated mortgage regulations, loan products like government-backed loans and new technologies like AI.

Such training keeps the employees in line with the compliance of laws like RESPA and TILA, they renew their licenses and are still competitive by following the industry best practices. Regular updates can be provided using e-learning modules, brief videos, and well-organized in-house training sessions.

Monitoring Performance & Behavior

To monitor efficiency and performance in the hiring of the mortgage sector, companies implement key performance indicators (KPIs), hardware such as a loan origination system (LOS) and customer relationship management (CRM) software, and automated monitoring systems to guarantee both output and conformity. Some of the most essential aspects revolve around measuring loan volume, conversion rates, and call quality alongside auditing fair lending risks and possible conflicts of interest.

Mortgage compliance is critical to success for mortgage professional, regulator, broker, Loan Officers, lenders or regulatory attorney. To manage regulatory compliance, firms should know how regulatory requirements affect business operations and adhere to industry best practices.

Record-Keeping & Documentation

Efficient record-keeping and documentation should entail the implementation of a systemized process that is aimed at gathering, checking and keeping records of the borrower’s details, lender’s documents and the transaction’s particulars with the view to maintaining the accuracy of the information that meets the set of rules and regulations and makes sure that the entire process is visible to all the interested parties.

Applicant documents such as pay stubs and tax returns, are among some of the things included in this procedure. Whereas, lender-specific documents like applications, disclosures and service agreements are also a part of it. A strong system depends on the thorough arrangement of records and their consistent and indefinite storage.

Responsibilities

- Review all executed recording documents for accuracy of the borrower’s signature, accuracy of the legal description and notary execution of the documents as required by each state.

- Confirm that all recording documents have been completed to meet the lender’s requirements.

- Submit recordable documents to the appropriate county for recording, either via e-record or by mailing them to the county.

- Scan loan packages, prepare certified true copies, and ship loan documents to lenders and borrowers. File documents and maintain file cabinets.

- Resolve recording issues and questions. Involving the Team Lead in all escalations is essential.

- Balance the file and identify shortages, set up recording refunds and verify the correct refund code has been applied.

- Manage daily workload by following the workflow for submitting documents for recording, noting the system and completing the required events.

- Perform other duties as assigned by management.

Compensation & Incentive Compliance in Hiring

Compensation and Incentive compliance in mortgage hiring is primarily governed by TILA, implemented through Regulation Z and RESPA, implemented through Regulation X. These rules are enforced by the Consumer Financial Protection Bureau (CFPB) to protect consumers from steering and unfair practices.

Perception of Compensation Restrictions

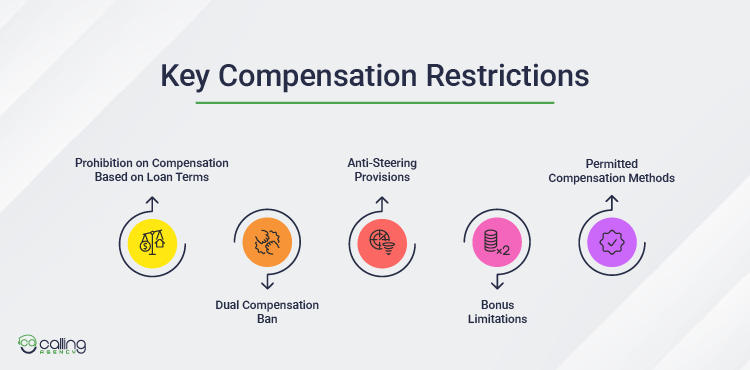

The Dodd-Frank Act is a law that sets rules for how people who help others get home loans (called loan originators or LOs) can be paid. This is to make sure that customers are not pushed into loans that can effect them financially. The rules are explained in Regulation Z.

According to these rules, LOs cannot be paid based on the loan’s terms, like the interest rate or fees. Also, LOs cannot get money from both the borrower and the lender for the same loan. Instead, they can be paid based on things like how many loans they help with, the quality of those loans, or a set salary.

Key Compensation Restrictions

- Prohibition on Compensation Based on Loan Terms

- Dual Compensation Ban

- Anti-Steering Provisions

- Bonus Limitations

- Permitted Compensation Methods

Structuring Incentives Safely

When it comes to structuring incentives, it is necessary to follow the rules very closely, mainly the SAFE Act and Regulation Z (Loan Originator Compensation Rule), in order to avoid situations where customers are directed to loans that are not convenient for them or that there is an implicit encouragement of that kind of unethical behavior.

Most of the measures implemented revolve around linking the incentives to indicators that are not influenced by the conditions of the loan (except for the amount) as well as encouraging general quality and compliance.

Examples

- Example 1: LO has an outstanding draw balance of $3,000 and has earned $3,500 in commissions but only has 1 active loan in the pipeline. The company will apply $3,000 to the advance balance and pay the LO the remaining $500.

- Example 2: LO has an outstanding draw balance of $3,000 and has earned $3,500 in commissions AND has 4 active loans in the pipeline. The company will apply $1,500 towards the balance due and pay the LO the remaining $2,000.

Compliant Incentive Structures

- Compensation Based on Overall Loan Volume

- Compensation Based on Lead Source

- Hourly Pay Rate

- Bonuses for Quality and Efficiency

- Fixed Payments per Loan

- Profit-Sharing Plans

- Non-Monetary Incentives

Monitoring for Compensation-Related Risk

- Interface with partners across Product, Capital Markets, Operations, MSR, and Sales in support of strategic business initiatives and continuous optimization of credit strategy.

- Monitor origination and portfolio performance to optimize risk-adjusted returns. Monitoring includes, but is not limited to, identifying deviations from expectations, diagnosing root cause and proposing corrective actions.

- Develop business cases and credit policy recommendations and coordinate approval and implementation through internal governance.

- Exercise strategic vision to identify and drive credit optimization efforts.

- Own and manage the monitoring of existing processes to identify improvements that contribute to a more effective and efficient operating environment.

- Provide an independent assessment of the quality, quantity, direction, and overall credit risk in the organization through planned reviews.

Here are several best practices organizations should consider when managing consumer compliance risk associated with Regulation Z and the fair lending regulations.

- Maintain written policy governing compensation.

- Document compensation plans by role and individual.

- Monitor Compliance.

Compliance Program Governance & Audit Framework

Keeping up with industry and state regulations is a necessary hurdle to success. Thankfully, compliance frameworks help you put pieces of the regulatory challenge together. Compliance Program Governance and Audit Framework is extremely important.

- Ensure Legal and Ethical Operations

- Mitigate Risks

- Promotes Trust

- Improves Efficiency

A Compliance Program Governance and Audit Framework helps a company ensure it adheres to laws and its own internal policies. This framework consists of three main components:

- Governance: This involves determining who is accountable for compliance and responsible for upholding the rules.

- Compliance Program: This encompasses establishing clear guidelines, providing employee training, and implementing strategies to mitigate risks.

- Regular Audits: These are evaluations that enable the company to assess its effectiveness in meeting compliance obligations.

Establish Written Policies & Procedures

Organizations can implement a Code of Conduct to outline how researchers and their teams can meet the goals, mission and ethical conduct of research. By ensuring the written policies and procedures are available to the relevant individuals in a centralized way, the requirements to meet the code of conduct are more transparent.

Steps to Establish Written Policies and Procedures

- Identify Applicable Laws and Regulations

- Conduct a Risk Assessment

- Define Scope, Purpose, Roles and Responsibilities

- Draft Policies and Detailed Procedures

- Establish Governance and Oversight Mechanisms

- Develop an Audit Framework

- Implement Reporting and Documentation Standards

- Communicate, Train and Enforce

- Monitor, Review and Improve

An effective compliance program has a comprehensive policy and standard documentation that focuses on crucial areas such as:

- Industry-Specific Requirements

- Conflict of Interest

- Ethics

- Data Privacy

- Anti-Corruption

Assign Accountability & Roles

Accountability for compliance and audit framework must be assigned across a clear governance structure, which involves the Board, senior management, dedicated compliance functions, internal audit and all employees.

A RACI (Responsible, Accountable, Consulted, Informed) matrix is a useful tool for documenting these roles.

| Role | Accountability | Responsibility | Consulted | Informed |

| Board of Directors/ Audit Committee | Overall governance, program oversight, and ultimate accountability for regulatory breaches | Approve the compliance charter/program and risk appetite; ensure adequate resources; monitor performance | CEO, CCO, Internal Audit, Legal Counsel | Regulators, External Auditors |

| Senior Management/ CEO | Ensuring all business operations comply with applicable laws and regulations; resource allocation | Champion a culture of compliance; set strategic direction; establish and maintain effective internal controls | CCO, Legal, Department Heads | Board, Employees |

| Chief Compliance Officer/ Compliance Function | Overseeing and managing daily compliance activities and program operations | Develop/implement policies and procedures; conduct risk assessments; manage training; monitor ongoing compliance; investigate issues; report to management and the Board | Internal Audit, Legal, HR, IT, Department Heads | Employees, Regulators |

| Internal Audit Function | Providing independent and objective assurance on the effectiveness of risk management and controls | Evaluate internal control design and effectiveness; conduct risk-based audits; report findings and recommendations to the Board/Audit Committee | CCO, Management, External Auditors | Board/Audit Committee |

| Department Heads/ Risk Owners | Compliance within their specific department’s operations | Implement compliance controls and procedures within their teams; ensure employee adherence; report potential issues to CCO | CCO, HR, Legal | Employees, Management |

| All Employees | Adhering to the code of conduct, policies, and procedures | Participate in training; report any potential misconduct or concerns through established channels (e.g., hotline) | Managers, CCO | N/A |

Audit, Testing & Remediation

A system of auditing and monitoring should be implemented in order to measure the effectiveness of the compliance program, ensure adherence to external regulations, and identify compliance risks.

Compliance programs should be reviewed regularly as part of normal operations; however, they should also be subject to a formal external audit. An audit should be performed at least on an annual basis. The auditor should provide a written report of their findings.

Audit Framework and Governance

- Governance Structure- This establishes compliance rules and appoints a compliance officer to meet legal requirements. Regular training promotes a compliance culture and periodic reviews evaluate effectiveness and highlight areas for improvement.

- Risk Assessment- A systematic compliance risk approach includes data collection, risk assessment based on impact and likelihood and categorizing risks by urgency and severity.

- Documentation and Policies- Needs clear documentation of policies, procedures and an audit trail for compliance efforts and incidents. It is essential to show regulators that compliance is maintained.

- Continuous Monitoring- It utilizes technology to offer real-time insight into compliance, facilitating the immediate detection and resolution of issues.

Regulatory Change Management

This framework is essential for governance and auditing, as it ensures compliance through a systematic approach that involves monitoring, impact assessment, stakeholder communication and continuous improvement.

This process is critical for mitigating risks such as fines and reputational damage and is often supported by technological solutions.

Aspects to Consider

- Clearly define which regulatory agencies and issuances apply to your organization globally, where it operates.

- Align your organization to existing applicable regulations.

- Monitor upcoming, in development and relevant regulatory activities that include investigations and enforcement, legislative activity and changes of existing applicable regulations.

- Understand the scope and impact of regulatory change on your existing policies and compliance program.

- Identify which processes and procedures may be and will be affected.

- Assessing risks and any changes to your organizational risk profile associated with the change.

- Adapting and implementing controls aligned to regulatory changes to mitigate those risks.

- Communicate applicable changes to all relevant stakeholders.

- Monitor the change to ensure it is being managed effectively.

- Review and update the change management plan as needed.

Third-Party and Vendor Considerations

When establishing rules and checks for a program to ensure that third parties and vendors comply with the law, it is essential to focus on a few key areas. First, conduct thorough risk assessments to understand potential vulnerabilities. Second, draft clear contracts that outline compliance requirements. Third, regularly monitor vendors and perform checks to ensure ongoing adherence to these standards. Lastly, implement robust security measures to safeguard data and information.

Having a good system to manage third-party risks is essential. This helps protect against problems like data leaks and makes sure that vendors follow legal rules and industry standards.

Practical Tips & Best Practices for Mortgage Hiring Compliance

To ensure that mortgage hiring practices comply with regulations, companies must incorporate key guidelines throughout the entire hiring process.

Best Practices

1. Master Regulatory Requirements

- Understand Key Laws

- Comply with Loan Originator Rules

- Stay Updated

2. Implement Fair and Consistent Hiring Processes

- Standardize Job Descriptions

- Use Inclusive Language

- Document Everything

3. Conduct Rigorous Due Diligence

- Verify NMLS Licenses

- Comprehensive Background Checks

- Verify Employment and Certifications

4. Foster a Culture of Compliance and Continuous Training

- Mandatory and Role-Specific Training

- Establish Internal Controls

- Encourage Open Communication

- Onboarding Program

5. Leverage Technology

- Compliance Software

- Secure Data Handling

Conclusion

Mortgage professionals will face a complex array of rules due to changes in federal laws, stricter state regulations and heightened marketing efforts. To navigate these challenges and remain compliant, lenders and loan officers must understand and adhere to RESPA regulations, particularly regarding co-marketing practices.

Ultimately, compliance is not just about avoiding penalties; it’s also about building and maintaining a reputable brand that can thrive in a highly competitive mortgage landscape. By embracing technology-driven compliance strategies, mortgage professionals can confidently market their services while staying within legal boundaries and ensure long-term success in an evolving industry.